The FMG Litmus Test

At the present time, government issued bond yields pretty much just give you your money back after inflation – if you’re lucky.

Often when you’re desperate for returns, you tend to ignore risk – which is what has been happening for a while now – and will likely continue well into the future, at least, that is, as long as central banks try to control the market through mere words and monetary deeds.

Yesterday, while stocks fell, gold bounced back from its recent losses. It’s now around US$1,330 an ounce – or $1,774 an ounce in Aussie dollars.

Many commentators with whom I agree have, for some time, been talking about “the coming correction in gold”, and this correction has been in the works for a while.

However, here’s another reason to like gold (and silver) in the longer term. Credit rating agency Standard and Poor’s (LINK) just released a disturbing new report showing projected corporate credit growth to 2020.

It expects corporate debt to expand by US$24 trillion over the next four years, thanks to low interest rates and what S&P describes as “ongoing central bank debt monetisation” – but, please, don’t ask me to explain that because, to be honest, I can’t. You’re just as capable of (mis)interpreting it as I am!

Anyway, not surprisingly, S&P expect the lions’ share of the new credit growth to come from China.

According to “The Daily Shot”, China’s share of the credit pie will climb to 43% from its current 35% and China will be responsible for 62% of all new credit growth.

In my respectful opinion, that’s a real risk, given that China’s corporate debt market is already massive. In fact, the S&P report states that more than half of the expected credit growth will come from already highly leveraged players.

It shouldn’t really be a surprise that a great deal (and a big percentage!) of this growth is coming from China. Why? Well, because corporates (and especially ‘state-owned enterprises’) borrow heavily in the knowledge that the government will bail them out if need be.

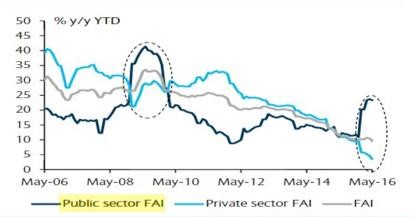

Right now, fear of default is not a big concern in China because it’s going through another one of its short lived growth spurts. However, as the chart below (from Haver Analytics, Barclays Research) shows, much of the recent growth is the result of a huge increase in government infrastructure spending.

That huge increase in government infrastructure spending is represented by the dark blue line, ie: ‘public sector FAI’, which stands for ‘fixed asset investment’.

If you’re wondering why, in recent times:

- the iron ore price has held up marginally; or

- the Aussie dollar has been so resilient,

this big spike in Chinese government fixed asset spending is your answer.

As the above chart illustrates, the spike is on par with the huge 2008/09 Chinese government initiated stimulus program that resulted in an iron ore boom and helped Australia avoid the worst of the global recession.

Maybe “Kevin ‘07” speaking a bit of Chinese motivated the Chinese government to initiate that stimulus program just for little old Australia! J

Anyway, that 2008/09 stimulus program didn’t last, and, in my opinion, neither will the current one!

Worryingly for Australia, this latest round of stimulus hasn’t really done too much. I believe that that’s because private sector investment continues to fall sharply – resulting in overall fixed asset investment declining as well.

So, what happens when the Chinese government’s latest stimulus efforts run out of steam?

It seems pretty obvious to me. In short, and far as Australia is concerned:

- iron ore prices will tumble back to their lowest of lows;

- the Aussie dollar will ‘head south’; and

- the Aussie government’s budget plans will again be under still further pressure.

We could still be a few months away from this reality though.

One market commentator for whom I have a great deal of time and respect likes to use Fortescue’s [ASX:FMG] share price as a barometer for the iron ore market. Right now it’s doing well and, in the last week or so, has traded between a range of about $4.00 and $4.50.

However, a fall back below $3.50 would, I think, indicate that its run is coming to an end.

It could be a warning that conditions are changing in the iron ore market – and that much lower prices are on their way.

So, keep an eye on FMG because, in my opinion, it will tell you quite a lot about Australia’s overall prospects in the months to come.

Also, don’t forget to look at your holdings of physical gold and silver – and also of ‘real’ (ie: folding) cash.

Peter Kerin

2 Responses to Shallow Chinese Stimulus